FORM FOUR BOOK KEEPING STUDY NOTES TOPIC 1-3.

Meaning of a Bill of Exchange

Define a bill of exchange

Bill

of exchange is written order letter in which there is not any

condition. Writer's sign will be in it. In this letter, order to other

person is given to pay the certain sum of money to the writer of letter

or to pay any other authorized person or who has this bill of exchange.

The Nature of Interest of a Bill of Exchange

Explain the nature of interest of a bill of exchange

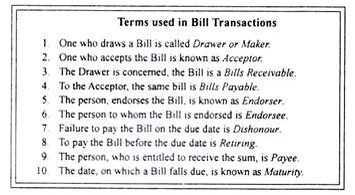

Essential of a Bill of Exchange

- It should be in written.

- Unconditional order to pay.

- Signed by writer.

- Debtor must be a certain person.

- Payment must be a certain amount.

- Payment must be done on maturity of bill.

- Acceptance must be given by debtor on this bill.

Bills

of Exchange and Promissory Notes are treated alike for accounting

purposes. That is, both are treated and recorded under the common

account “Bills of Exchange”.

We come across four parties to a Bill:

- (a) Drawer,

- (b) Drawee (Acceptor),

- (c) Endorser, and

- (d) Endorsee.

When

a drawer endorses a Bill, which he received from the Acceptor, he

becomes Endorser. Endorsee is a person to whom the Bill is transferred.

When the endorsee, again, endorses the Bill, he becomes an Endorser and

the receiver of the endorsed Bill is an Endorsee.

A

bill of exchange or Promissory Note may be treated as Bills Receivable,

when payment has to be received against it. Thus, a bill of exchange is

Bills Receivable for the drawer as he has to receive the amount. A bill

of exchange or Promissory Note may be treated as a Bill Payable, when

payment has to be made against it.

Thus,

a bill of exchange is a Bill Payable for the drawee (Acceptor). Thus,

it is clear that Bills of Exchange or Promissory Notes can be Bills

Receivable to one party and Bills Payable to another party.

The Bill in the possession of the Creditor may be dealt with in any one of the following ways:

- One can keep the Bill till the date of maturity and realize the payment against it.

- One can discount the Bill with a bank before its maturity, if he is in need of money.

- One can transfer the Bill, against a debt, to his Creditor by endorsing it.

- One can send the Bill to the bank for collection of amount against it.

We shall discuss the accounting treatment of transactions:

Bill Recieved

Account for bill received

Accrued Interest; Default of Bill; Default or Dishonor ; The Discounting of a Bill of Exchange

Account for: Accrued interest; Default of bill; Default or dishonor; The discounting of a bill of exchange

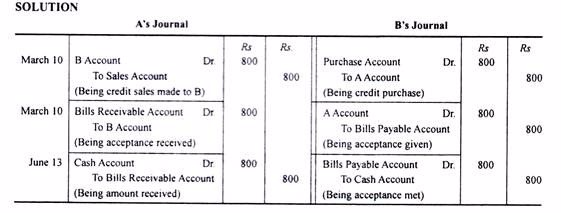

Drawing, Accepting and Discharge of A Bill:

Illustration 1:

On

March 10th, A sold goods to B and draws on B a Bill at three months for

Rs 800, which B accepts immediately and returns it to A. The Bill is

honoured on the due date. Pass entries in the books of both A and B.

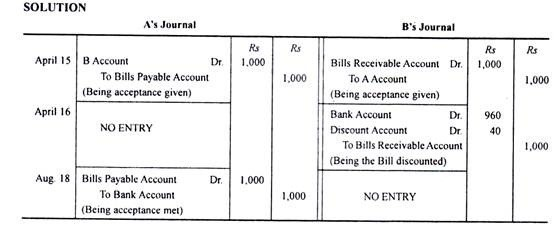

Discounting the Bill:

Illustration 2:

A

accepted a four months’ draft for Rs 1,000 drawn on him by B on 15th

April. The Bill was discounted with the bankers on the next day at 12%.

On maturity the Bill was met. Make journal entries in the books of A and

B.

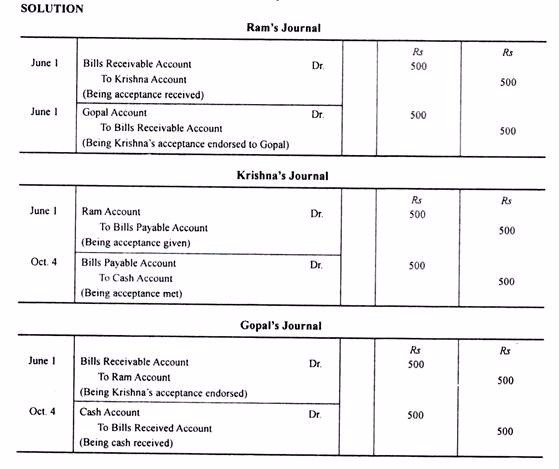

Endorsing the Bill:

On

1st June Ram drew a bill upon Krishna for Rs 500 at four months date.

This was duly accepted and payable at Canada Bank. After the acceptance,

the Bill was endorsed to Gopal. On the due date, the Bill was honoured.

Pass the journal entries in the books of all parties.

Dishonouring the Bill:

(a) When Drawer is the Holder of the Bill:

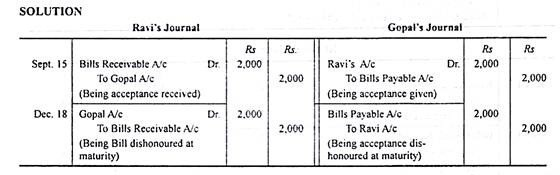

Illustration 4:

Mr.

Ravi draws a Bill for Rs 2,000 on Gopal on 15th September for three

months. On maturity, Gopal failed to honour the Bill. Pass the necessary

journal entries in the books of Ravi and Goipal, if he had retained the

Bill with him till maturity. (Calicut)

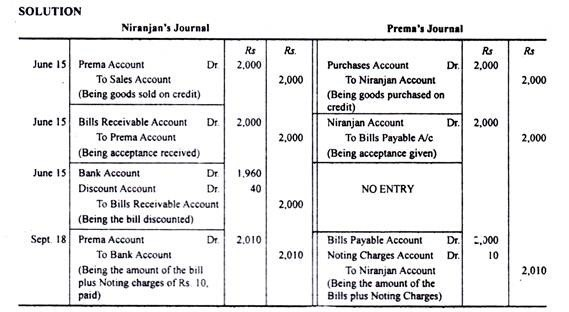

(b) When Banker is the Holder of the Bill:

On

15th June, Niranjan sold goods to Prema, valued at Rs 2,000. He drew a

Bill at 3 months for the amount and discounted the same with his bankers

at Rs 1,960. On the due date, the Bill was dishonoured and Niranjan

paid the bank the amount due plus the noting charges of Rs 10. Pass the

journal entries in the books of the two parties. (B.Com Mysore)

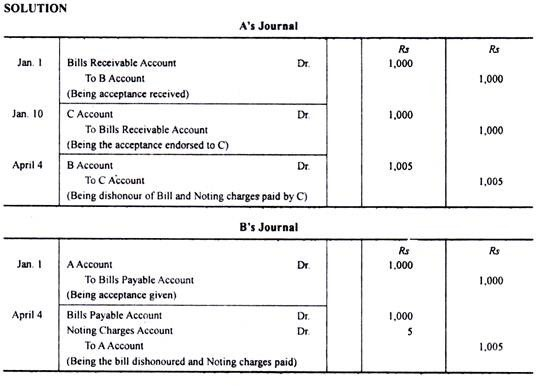

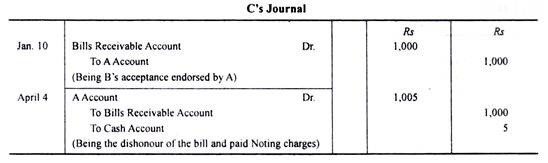

(c) When Endorse is the Holder of the Bill:

On

1st January, A drew a Bill on B for Rs 1,000 payable after three

months. B accepted the bill and returned it to A. After 10 days A

endorsed the Bill to his Creditor C.

On

the due date, the Bill was dishonoured and C paid Rs 5 as noting

charges. Record the transactions in the journals of A, B and C.

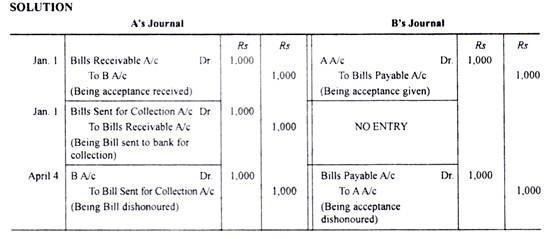

(d) When the Bill is Sent for Collection:

Illustration 6:

On

1st January, A drew a bill on B for Rs 1,000, payable after three

months. Immediately after its acceptance, A sent the Bill to his Bank

for collection. On the due date, the Bill was dishonoured.

Record the transactions in the journals of A and B.

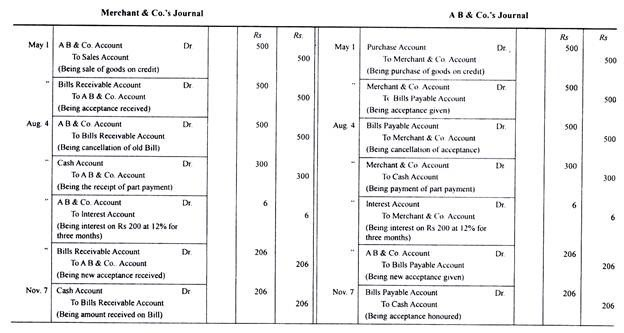

Renewal of the Bills:

Illustration 7:

On

1st May, Merchant & Company sold goods to A B & Co. for Rs 500

and drew upon him a Bill at three months for the amount. A B & Co.

accepted the draft and returned to Merchant & Co. On the due date A B

& Co. expressed their inability to meet the Bill and offered Rs 300

in cash and to accept a new bill for the balance plus interest at 12%

p.a. for three months. Merchant & Co. agreed to the proposal. On

maturity, the bill was duly met by A B & Co.

Pass entries in the books of the parties to record the above transactions. (B. Com., Karnataka, Madras)

Solution:

Effects of Dishonour of a Bill:

- When a bill is dishonoured, it becomes valueless and the original position of debtor and creditor is restored between the drawee and the drawer.

- Upon its dishonor, the holder of a bill has a right of action against the drawee or any previous endorser.

- When an endorser makes the payment to the endorsee, he can sue any previous endorser or the drawer.

- Upon dishonour, to avoid confusion and multiplicity of legal actions, generally the drawer takes up the bill and exercises his rights upon the drawee.

- Expenses incurred for establishing the fact of dishonour of a bill (noting charges) are generally paid by the holder, but ultimately these are recoverable from the drawee.

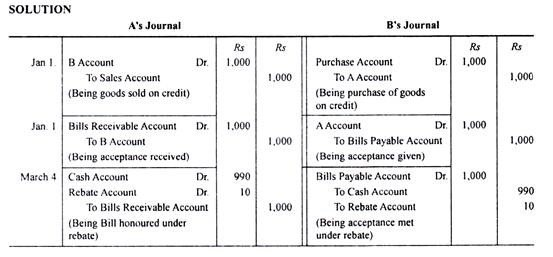

Retiring a Bill under Rebate:

Illustration 8:

On

1st January, A sold goods to B for Rs 1,000 and drew upon him a Bill at

three months for the amount. B accepted the Bill and returned it to A.

On 4th March, B returned the Bill under rebate of 12% p a.

Record these transactions in the journals of A and B.

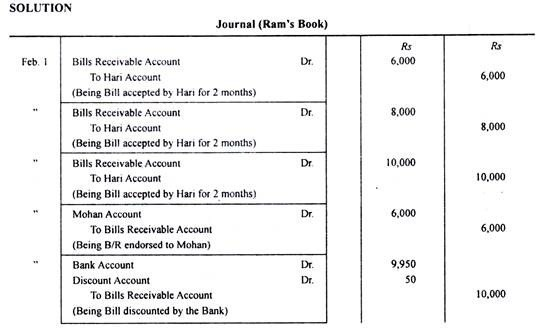

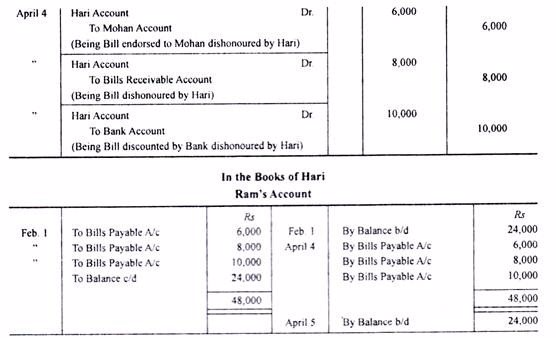

Illustration 9:

On

1st February, Ram received from Hari three acceptances for Rs 6,000, Rs

8,000 and Rs 10,000 for two months.The first Bill for Rs 6,000 was

endorsed to Mohan; the second Bill for Rs 8,000 was held till due date;

and the third Bill for Rs 10,000 was discounted for Rs 50.At maturity

all the Bills were dishonored. Give journal entries in the books of Ram

and the ledger accounts in the books of Hari, in respect of these

transactions. (CA)

Journalise the following transaction in the books of Nilesh.

- (a) Naresh informs Nilesh that Snajay’s acceptance for `. 8,000 endorsed to Naresh has been dishonoured. Noting charges `. 200.

- (b) Sujit renews his acceptance to Nilesh for `. 4,800 by paying `.1,600 in cash and accepting a new bill for the balance plus interest for 3 months @12% p.a.

- (c) Prakash’s acceptance to Nilesh for `.24,000 retired one month before its due date at a discount of 12% p.a.

- (d) Bank informs Nilesh, the dishonour of Prashant’s acceptance for `. 8,000, discounted with Bank. Noting charges `.160.

Journal of Nilesh

| Date | Particulars | LF | Debit (`.) | Credit (`.) |

| Sanjay A/c…………………………..Dr. To Naresh A/c(Being endorsed bill dishonoured and noting charges paid) | 8,200 | 8,200 | ||

| Sujit A/c………………………………Dr. To Bills Receivable A/c(Being Bills cancelled) | 4,800 | 4,800 | ||

| Sujit A/c………………………………Dr. To Interest A/c(Being interest receivable) | 96 | 96 | ||

| Cash A/c……………………………..Dr. To Sujit A/c(Being part payment received) | 1,600 | 1,600 | ||

| Bills Receivable A/c………………..Dr. To Sujit A/c(Being new bill drawn and accepted due after 3 months) | 3,296 | 3,296 | ||

| Cash A/c………………………………Dr.Discount A/c…………………………Dr. To Bills Receivable A/c(Being Bill Retired) | 23,760240 | 24,000 | ||

| Prashant A/c…………………………Dr. To Bank A/c(Being discounted bill dishonorued and noting charges paid) | 8,160 | 8,160 |

A bill of Exchange with Interest Charges included in the Face Amount

Account for a bill of exchange with interest charges included in the face amount

The Concept of Present Value in Accounting of a Log-term Bill of Exchange

TOPIC 2: JOINT VENTURES

The Meaning of Joint Venture

Define a joint venture

An

association of two or more individuals or companies engaged in a

solitary business enterprise for profit without actual partnership or

incorporation; also called a joint adventure.

A

joint venture is a contractual business undertaking between two or more

parties. It is similar to a business partnership, with one key

difference: a partnership generally involves an ongoing, long-term

business relationship, whereas a joint venture is based on a single

business transaction. Individuals or companies choose to enter joint

ventures in order to share strengths, minimize risks, and increase

competitive advantages in the marketplace. Joint ventures can be

distinct business units (a new business entity may be created for the

joint venture) or collaborations between businesses. In collaboration,

for example, a high-technology firm may contract with a manufacturer to

bring its idea for a product to market; the former provides the

know-how, the latter the means.

Joint Venture Accounts in the Books of the Parties

Show the joint venture accounts in the books of the parties

Joint Venture Memorandum Account .

The

is another method to record the transactions in the books of the

various parties. Under this method the joint venture account is prepared

on memorandum basis, just to find out the profit or loss but not as a

part of financial books. The name of such account is memorandum joint venture account. I books only one account is opened styled as "joint venture with.....account".

Suppose

A and B have entered into a joint venture. The A will open an account

named, joint venture with B account. Similarly, B will open, in his

books, joint venture with A account. This account is prepared in the

following manner:-

- Goods sent or expenses incurred on joint venture are debited to the account.

- No account is taken of goods supplied or expenses incurred on joint venture by the other party.

- If any cash or acceptance is received on account of joint venture or from other party, this account is credited.

- The account is debited with own share of profit (ascertained by the memorandum joint venture account) the credit being given to profit and loss account. If there is a loss the profit and loss account is debited and this account is credited. The balance of this account will show either the amount owing to the other party or amount owned by the other party.

Example 1

Example:

Following example will make the concept more clear:

Memorandum Joint Venture Account

| Debit Side | Credit Side | |||

| $ | $ | |||

| To A (Cost of goods & Exp.) | 5,400, | By B - sales | 12,000 | |

| To B (Cost of goods & Exp.) | 4,300 | |||

| To B (Commission) | 600 | |||

| To Profit: | ||||

| A 4/5 | 1,360 | |||

| B 1/5 | 340 | |||

| 1,700 | ||||

| 12,000 | 12,000 | |||

In the Books of A

Joint Venture With B Account

| Debit Side | Credit Side | ||

| $ | $ | ||

| To Cash (goods) | 5,400, | By Cash | 6,760 |

| To Cash (Expenses) | 4,300 | ||

| To Profit and loss (4/5 of profit) | 1,360 | ||

| 6,760 | 6,760 | ||

In the Books of B

Joint Venture With A Account

| Debit Side | Credit Side | ||

| $ | $ | ||

| To Cash (goods) | 4,000 | By Cash | 12,000 |

| To Cash (Expenses) | 300 | ||

| To Commission | 600 | ||

| To Profit and loss (1/5 of profit) | 340 | ||

| To Cash | 6,760 | ||

| 12,000 | 12,000 | ||

Problem 1 - Journal Entries, Joint Venture Account Co-venture Accounts:

A

and B were partners in a joint venture sharing profits and losses in

the proportion of four-fifth and one-fifth respectively. A supplies

goods to the value of $5,000 and inures expenses amounting to $400. B

supplies goods to the value of $4,000 and his expenses amounting to

$300. B sells goods on behalf of the joint venture and realizes $12,000.

B is entitled to a commission of 5 percent on sales. B settles his

accounts by bank draft.

Required: Give journal entries and necessary ledger accounts in the books of both the parties.

Solution:

Books of A

Journal Entries

| joint venture account | 5,000 | |

| To Cash account | 5,000 | |

| (Goods sent to B) | ||

| joint venture account | 400 | |

| To Cash account | 400 | |

| (Expenses incurred on goods sent to B) | ||

| joint venture account | 4,000 | |

| To B | 4,000 | |

| (Goods supplied by B) | ||

| Joint venture account | 300 | |

| To To B | 300 | |

| (Expenses incurred by B on joint venture) | ||

| B | 12,000 | |

| To Joint venture account | 12,000 | |

| (Sales proceeds received by B) | ||

| Joint venture account | 600 | |

| To B | 600 | |

| (Commission due to B on sales at the rate of 5%) | ||

| Joint venture account | 1,700 | |

| To B | 340 | |

| To Profit and loss account | 1360 | |

| (Profit $1,700 divided as 1/5 to B and 4/5 to self) | ||

| Cash account | 6,760 | |

| To B | 6,760 | |

| (The draft received from B in settlement) | ||

Joint Venture Account

| Debit Side | Credit Side | ||

| To Cash - Goods | 5,000 | By B - Sales | 12,000 |

| To Cash - Expenses | 400 | ||

| To B - Goods | 4,000 | ||

| To B - Expenses | 300 | ||

| To B - Commission | 600 | ||

| To B - Share of profit | 340 | ||

| To Profit and loss account | 1,360 | ||

| 12,000 | 12,000 | ||

B Account

| Debit Side | Credit Side | ||

| To Joint venture account | 12,000 | By Joint venture - Goods | 4,000 |

| By Joint venture - Expenses | 300 | ||

| By Joint venture - Commission | 600 | ||

| By Joint venture - Profit | 340 | ||

| By Cash | 6,760 | ||

| 12,000 | 12,000 | ||

Books of B Journal Entries

| joint venture account | 4,000 | |

| To Cash account | 4,000 | |

| (The value of goods supplied) | ||

| joint venture account | 300 | |

| To Cash account | 300 | |

| (Expenses incurred on joint venture) | ||

| joint venture account | 5,000 | |

| To A | 5,000 | |

| (Goods supplied by A) | ||

| Joint venture account | 400 | |

| To A | 400 | |

| (Expenses incurred by B on joint venture) | ||

| Cash account | 12,000 | |

| To Joint venture account | 12,000 | |

| (Sales proceeds received in cash) | ||

| Joint venture account | 600 | |

| To Commission account | 600 | |

| (Commission due on sales at the rate of 5%) | ||

| Joint venture account | 1,700 | |

| To A | 340 | |

| To Profit and loss account | 1360 | |

| (Profit $1,700 divided as 1/5 to B and 4/5 to A) | ||

| A | 6,760 | |

| To Cash account | 6,760 | |

| (The draft sent to A in settlement) | ||

Joint Venture Account

| Debit Side | Credit Side | ||

| To Cash - Goods | 4,000 | By Cash account - Sales | 12,000 |

| To Cash - Expenses | 300 | 0 | 0 |

| To A - Goods | 5,000 | ||

| To A - Expenses | 400 | ||

| To Commission | 600 | ||

| To A - Share of profit | 1,360 | ||

| To Profit and loss account | 340 | ||

| 12,000 | 12,000 | ||

A Account

| Debit Side | Credit Side | ||

| To Cash account | 6,760 | By Joint venture account | 5,000 |

| By Joint venture - Expense | 400 | ||

| By Joint venture - profit | 1,360 | ||

| 6,760 | 6,760 | ||

Problem 2 - Joint Venture Account and Co-venturer Accounts:

Salim

& Sons bought goods of the value of $7,500 and consigned them to

Tahir and Co. to be sold to them on a joint venture, profit being

divided in 2/3 : 1/3. They also paid $550 for freight, insurance and

cartage and drew on Tahir and Co. for $3,000 on account. The bill was

discounted by Salim & Sons for $2,900. Tahir and Co. paid $300 for

dock dues, storage, rent etc. The sales realised $12,500 and the sales

expenses $250 were defrayed by Tahir and Co. The later forwarded a sight

draft for the balance due to Salim & Sons after charging their

sales commission at 5 percent on the gross proceeds.

Required: Write up the accounts in the books of both the parties. No interest need to be brought into account.

Solution:

Salim & Sons Books

Joint Venture Account

| Debit Side | Credit Side | |||

| $ | $ | |||

| To cash - cost of goods | 7,500 | By Tahir & Co.-sales proceeds | 12,500 | |

| To cash - expenses | 550 | |||

| To Discount on bill | 100 | |||

| To Tahir and Co. | ||||

| Dock, dues & storage | 300 | |||

| Sales expenses | 250 | |||

| Commission | 625 | |||

| 1,175 | ||||

| To Profit and loss - 2/3 share | 2,116.67 | |||

| To Tahir & Co. - share of profit | 1,058.33 | |||

| 12,500 | 12,500 | |||

Tahir & Co.

Joint Venture Account

| Debit Side | Credit Side | |||

| $ | $ | |||

| To Salim & Co. - cost of goods | 7,500 | By Cash - sales proceeds | 12,500 | |

| To Salim & Co. - expenses | 550 | |||

| To Salim & Co. - Discount on bill | 100 | |||

| To Cash. | ||||

| Dock, dues & storage | 300 | |||

| Sales expenses | 250 | |||

| 1,175 | ||||

| Commission | 625 | |||

| To Profit and loss - 1/3 share | 1,058.33 | |||

| To Salim & Co. - share of profit | 2,116.67 | |||

| 12,500 | 12,500 | |||

Salim & Sons

| Debit Side | Credit Side | ||

| $ | $ | ||

| To Bills payable a/c | 3,000 | By Joint venture account | 7,500 |

| To Cash - sight draft | 7,266.67 | By Joint venture account | 550 |

| By Discount account | 100 | ||

| By Joint venture account - 2/3 | 2,116.67 | ||

| 10,266.67 | 10,266.67 | ||

The Profit or Otherwise of the Joint Venture

Determine the profit or otherwise of the joint venture

Advantages of Joint Ventures

are speed, access, sharing of resources and the leveraging of

underutilized resources, high profits, back end income, low or no risk

opportunities and massive leverage.

Disadvantages of Joint Ventures

are the possibility of being ripped off or disappointed by unscrupulous

and unprofessional JV partners, and hurting your reputation and/or

customers and associates by associating with the wrong people, even

unknowingly.

TOPIC 3: CONSIGNMENT

The Account in the Consignors and Consignee’s Books

Show the account in the consignors and consignee’s books

Consignment Overview

Consignment

occurs when goods are sent by their owner (the consignor) to an agent

(the consignee), who undertakes to sell the goods. The consignor

continues to own the goods until they are sold, so the goods appear

asinventoryin the accounting records of the consignor, not the

consignee.

Consignment Accounting - Initial Transfer of Goods

When

the consignor sends goods to the consignee, there is no need to create

an accounting entry related to the physical movement of goods. It is

usually sufficient to record the change in location within the inventory

record keeping system of the consignor. In addition, the consignor

should consider the following maintenance activities:

- Periodically send a statement to the consignee, stating the inventory that should be on the consignee's premises. The consignee can use this statement to conduct a periodic reconciliation of the actual amount on hand to the consignor's records.

- Request from the consignee a statement of on-hand inventory at the end of each accounting period when the consignor is conducting a physical inventory count. The consignor incorporates this information into its inventory records to arrive at a fully valued ending inventory balance.

- It may also be useful to occasionally conduct an audit of the inventory reported by the consignee.

From

the consignee's perspective, there is no need to record the consigned

inventory, since it is owned by the consignor. It may be useful to keep a

separate record of all consigned inventory, for reconciliation and

insurance purposes.

Consignment Accounting - Sale of Goods by Consignee

When

the consignee eventually sells the consigned goods, it pays the

consignor a pre-arranged sale amount. The consignor records this

prearranged amount with a debit to cash and a credit to sales. It also

purges the related amount of inventory from its records with a debit to

cost of goods sold and a credit to inventory. A profit or loss on the

sale transaction will arise from these two entries.

Depending

upon the arrangement with the consignee, the consignor may pay a

commission to the consignee for making the sale. If so, this is a debit

to commission expense and a credit to accounts payable.

From

the consignee's perspective, a sale transaction triggers a payment to

the consignor for the consigned goods that were sold. There will also be

a sale transaction to record the sale of goods to the third party,

which is a debit to cash or accounts receivable and a credit to sales.

Consignment

is a term used to refer to an arrangement whereby goods are sent by

their owner (consignor) to an agent (consignee) who holds and sells the

goods on behalf of the owner for a commission. It is important to

understand that the agent never owns the goods.

Distinction/Difference Between Consignment and Sale:

The following are the main points of the difference between consignment and sale.

Transfer of Legal Ownership of the Goods:

In case of sale, the legal ownership of the goods sold is transferred

to the purchaser of goods. Whereas in case of a consignment of goods ,

the legal ownership of the goods is not transferred to the consignment

but the ownership of the goods remains vested in the consignor till the

goods consigned are sold by the consignee.

Relationship Between Consignor and Consignee:

In case of a sale of goods, the relationship between the seller and the purchaser of the goods is that of a creditor and a debtor whereas in case of a consignment the relationship between the consignor and the consignee is that of a principal and agent. Because the consignee is to sell goods on behalf of the consignor.

Expenses Incurred:

In

consignment, expenses incurred by the consignee in connection with the

goods consigned to him are usually borne by the consignor whereas in

case of a sale, expenses incurred after sale of goods are born by the

purchaser.

Risk Attached to the Goods:

In case of consignment, risk attached to the goods sold lies with the consignor till the goods consigned are sold by the consignee. But in case of a sale, risk attached to the goods sold is transferred to the buyer of goods.

Return of Goods:

In

case of consignment, return of goods is possible if the goods are not

sold by the consignee. But in case of sale, return of goods is not

possible as goods once sold are not returnable.

Requirement of Account Sale:

In case of consignment, account sale

is required to be submitted periodically by the consignee to the

consignor. But in case of sales no account sale is required to be

submitted by the purchaser to the seller.

Problem 1 (Journal Entries and Ledger Accounts):

Riaz

Sugar Factory of Multan, consigned to Mr. Shahid of Lahore 400 bags of

sugar at $25 per bag. They also paid cartage, freight, etc. $250. The

consignor drew on consignee as an advance against the consignment at 3

months for $6,000 which they discounted at their bank at 5 percent. The

consignee sold off the goods and rendered an account sales showing that

the goods realized $12,000, out of which he deducted his charges

amounting to $80 and his commission at 5 percent.

Required: Make journal entries in respect of the above transactions in the books of consignor as well as the consignee

Solution:

Consignor's Books

JOURNAL ENTRIES

| Dr. | Cr. | |

| $ | $ | |

| Consignment to Lahore account | 10,000 | |

| To Goods sent on consignment account | 10,000 | |

| Consignment to Lahore account | 250 | |

| To Bank account | 250 | |

| Bills receivable account | 6,000 | |

| To Shahid Ali | 6,000 | |

| Bank account | 5,925 | |

| Discount account | 75 | |

| To Bills receivable account | 6,000 | |

| Shahid Ali | 12,000 | |

| To Consignment to Lahore account | 12,000 | |

| Consignment to Lahore account | 680 | |

| To Shahid Ali | 680 | |

| Bank | 5320 | |

| To Shahid Ali | 5320 | |

| Consignment to Lahore account | 1,070 | |

| To Profit and loss account | 1,070 | |

| Goods sent on consignment account | 10,000 | |

| To Trading account | 10,000 |

LEDGER ACCOUNTS

Consignment to Lahore Account

| $ | $ | ||

| Dr. | Cr. | ||

| To Goods sent on consignment | 10,000 | By Shahid Ali - Sales Proceeds | 12,000 |

| To Bank expenses | 250 | ||

| To Shahid Ali | 680 | ||

| To Profit and loss account | 1,070 | ||

| 12,000 | 12,000 |

Goods Sent on Consignment Account

| $ | $ | ||

| Dr. | Cr. | ||

| To Trading account | 10,000 | By Consignment to Lahore | 10,000 |

Bank Account

| Dr. | Cr. | ||

| $ | $ | ||

| To Bills receivable | 5,925 | By Consignment to Lahore | 250 |

| To Shahid Ali | 5,320 |

Shahid Ali (Consignee)

| Dr. | Cr. | ||

| $ | $ | ||

| To Consignment to Lahore | 12,000 | By Bills receivable | 6,000 |

| By Consignment to Lahore | 680 | ||

| By Bank account | 5,320 | ||

| 12,000 | 12,000 |

Bills receivable Account

| Dr. | Cr. | ||

| $ | $ | ||

| To Shahid Ali | 6,000 | By Bank | 5,925 |

| By Discount | 75 | ||

| 6,000 | 6,000 |

Discount Account

| Dr. | 0 | Cr. | 0 |

| 0 | $ | 0 | $ |

| To Bills receivable | 75 | By Profit and loss account | 75 |

Profit and Loss Account

| Dr. | Cr. | ||

| $ | $ | ||

| By Consignment to Lahore | 1,070 |

Trading Account

| Dr. | Cr. | ||

| $ | $ | ||

| By Goods sent on consignment | 10,000 |

Consignee's Books

JOURNAL ENTRIES

| Dr. | Cr. | |

| $ | $ | |

| Riaz sugar factory | 6,000 | |

| To Bills payable account | 6,000 | |

| Riaz sugar factory | 80 | |

| To Bank account | 80 | |

| Bank account | 12,000 | |

| To Riaz sugar factory | 12,000 | |

| Riaz sugar factory | 600 | |

| To Commission account | 600 | |

| Riaz sugar factory | 5,320 | |

| To Bank account | 5,320 | |

| Bills payable | 6,000 | |

| To Bank account | 6,000 |

LEDGER ACCOUNTS

Riaz Sugar Factory (Consignor)

| Dr. | Cr. | ||

| $ | $ | ||

| To Bills payable | 12,000 | By Bank account | 12,000 |

| To Bank - expenses | 80 | ||

| To Commission | 600 | ||

| To Bank - Balance | 5,320 | ||

| 12,000 | 12,000 |

Bank Account

| Dr. | Cr. | ||

| $ | $ | ||

| To Riaz sugar factory | 12,000 | By Riaz sugar factory | 80 |

| By Riaz sugar factory | 5,320 | ||

| By Bills payable | 6,000 |

Commission Account

| Dr. | Cr. | ||

| $ | $ | ||

| To Profit and loss account | 600 | By Riaz sugar factory | 600 |

Bills Payable Account

| Dr. | Cr. | ||

| $ | $ | ||

| To Bank | 6,000 | By Riaz sugar factory | 6,000 |

Problem 2 - (Abnormal Loss):

1,000

Motors were consigned by A & Co., of Lahore to Bashir of Karachi at

an invoice cost of $150 each. A & Co., paid freight $10,000 and

insurance $1,500. During transit 100 motors were completely destroyed.

Bashir took delivery of the remaining motors and paid $14,400 as duty.

Bashir

sent a bank draft to A & Co., for $50,000 as an advance payment and

later sent an account sale showing that 800 motors were sold at $220

each. Expenses incurred by Bashir on godown rent and advertisement etc.,

amounted to $2,000. Bashir is entitled to commission of 5 per cent.

Required:

Prepare consignment account and Bashir's account in the books of A

& Co., assuming that nothing has been recovered from the insurance

company due to defect in the policy.

Solution

Consignment to Karachi Account

| $ | $ | ||

| To Goods sent on consignment | 1,50,000 | By sales (800 × 220) | 1,76,000 |

| To Bank - freight and insurance | 11,500 | By Profit and loss account - Ab. Loss* | 16,150 |

| To Bashir - duty | 14,400 | By Stock on consignment** | 17,750 |

| To Bashir - expenses | 2,000 | ||

| To Bashir - commission | 8,800 | ||

| To Profit and loss account | 23,200 | ||

| 2,09,900 | 2,09,900 |

Bashir

| $ | $ | |||

| To Consignment account | 1,76,000 | By Bank | 50,000 | |

| By Consignment account | ||||

| Duty | 14,400 | |||

| Expenses | 2,000 | |||

| 16,400 | ||||

| By Consignment account-commission | 8,800 | |||

| By Balance c/d | 1,00,800 | |||

| 1,76,000 | 1,76,000 | |||

Working Note:

| (1) | *Calculation of abnormal loss: | |

| 100 motors at $150 each | $15,000 | |

| Add 100/1000 of freight and insurance (11,500 × 100/1000) | 1,150 | |

| Abnormal loss | 16,150 | |

| (2) | **Calculation of Closing Stock: | |

| 100 motors at $150 each | $15,000 | |

| Add 100/1000 of freight and insurance (11,500 × 100/1000) | 1,150 | |

| 100/900 of duty | 1,600 | |

| Closing stock or unsold stock | 17,750 |

Problem 3 (Invoicing Goods Higher Than Cost):

Rashid

of city A sends 100 sewing machines on consignment to Malik of city B.

The cost of each machine is $130 but the invoice price is at the rate of

$160 each. Rashid spends $400 on packing and despatch. Malik receives

the consignment and immediately accepts Rashid's draft for $8000.

Subsequently, Malik informs Rashid that 80 machines have been sold at

$175 each. Expenses paid by Malik are; freight $600, godown rent $50,

and insurance $100. Malik is entitled to a commission of 6 per cent on

sales and 1-1/2 percent as del credere commission.

Give journal entries in the books of Rashid . Also prepare necessary ledger accounts:

Solution:

Journal

| Consignment to city B | 16,000 | |

| To Goods sent on consignment account | 16,000 | |

| (100 machines at $160 each sent on consignment) | ||

| Consignment to city B | 400 | |

| To Cash account | 400 | |

| (Expenses incurred on consignment) | ||

| Bills receivable account | 8,000 | |

| To Malik | 8,000 | |

| (Malik's acceptance received) | ||

| Malik | 14,000 | |

| To Consignment to city B account | 14,000 | |

| (80 machine's sold Malik at $175 each) | ||

| Consignment to city B account | 750 | |

| To Malik | 750 | |

| (Expenses incurred) | ||

| Consignment to city B account | 1,050 | |

| To Malik | 1,050 | |

| (Commission at 6% plus 1-1/2 on sales) | ||

| Consignment to city B account | 600 | |

| To Stock reserve account | 600 | |

| (Difference in closing stock adjusted) | ||

| Stock on consignment account | 3,400 | |

| To Consignment to city B account | 3,400 | |

| (Value of 20 machines in the hands of Malik) | ||

| Goods sent on consignment account | 3,000 | |

| To Consignment to city B account | 3,000 | |

| (The difference in the invoice value and cost, $30 per machine adjusted) | ||

| Goods sent on consignment account | 13,000 | |

| To Trading account | 13,000 | |

| (Transfer of goods sent on consignment to trading account) | ||

| Consignment to city B account | 1,600 | |

| To Profit and loss account | 1,600 | |

| (Transfer of profit on consignment) |

Consignment to City B Account

| $ | $ | |||

| To Goods sent on consignment | 16,000 | By Malik - Sales proceed | 14,000 | |

| To Cash - Expenses | 400 | By Stock on consignment | 3,400 | |

| To Malik - Expenses: | By Goods sent on consignment | 3,000 | ||

| Freight | 600 | |||

| Rent | 50 | |||

| Insurance | 100 | |||

| 750 | ||||

| To Malik - Commission | 1,050 | |||

| To Consignment stock reserve | 600 | |||

| To Profit and loss account | 1,600 | |||

| 20,400 | 20,400 | |||

Malik

| $ | $ | ||

| To Consignment to city B account | 14,000 | By Bills receivable account | 8,000 |

| By Consignment to city B account | |||

| Expenses | 750 | ||

| Commission | 1,050 | ||

| By Balance c/d | 4,200 | ||

| 14,000 | 14,000 |

The Transfer of the Consignee’s and Consignee’s Accounts to the Profit and Loss Account

Show the transfer of the consignee’s and consignee’s accounts to the profit and Loss Account

Profit and Loss Account

| Dr. | Cr. | ||

| $ | $ | ||

| By Consignment to Lahore | 1,070 |

Preparation of the Accounts Sales

Prepare the Accounts sales

Activity 1

Prepare the Accounts sales

The Consignment Inward Account in the Book of the Consignee

Show the consignment Inward Account in the book of the Consignee

Activity 2

Show the consignment Inward Account in the book of the Consignee

No comments